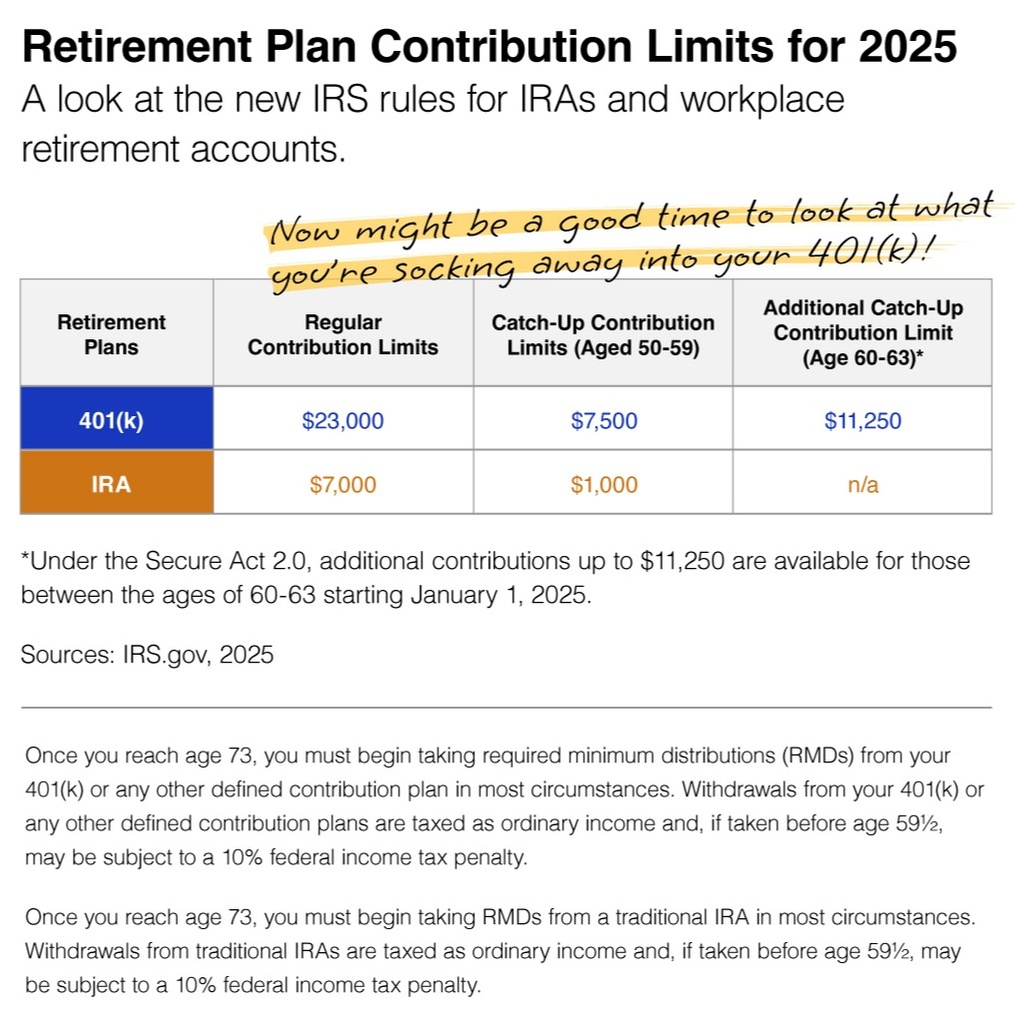

Retirement Plan Contribution Limits for 2025

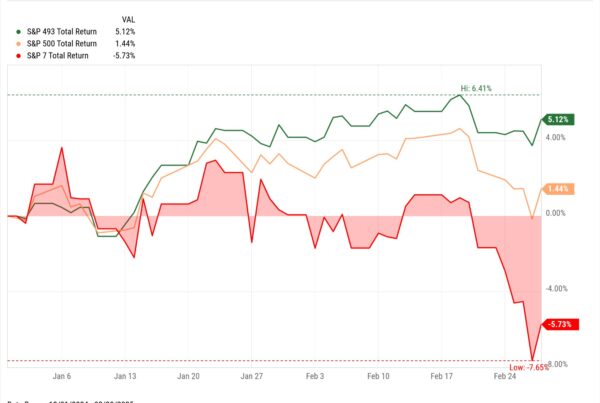

Though the S&P 500 is up 1.4% through the end of February, it’s the broader “S&P 493” that is keeping the index afloat, while the Magnificent Seven have entered a selloff phase. This shift signals a potential market rotation, where leadership moves away from the largest tech names toward broader opportunities.

For those who are currently participating in workplace plans like a 401(k) or 403(b), this offers an opportunity to invest more into your current retirement strategy. Especially if you are looking to max out your plan limits, it may be a good idea to take another look at your contribution amounts in 2025.